Long Call Payoff Diagram — Series 7 Cheat Sheet & Full Walkthrough

Updated April 2026 · 6 min read · Part of the Series 7 Options Crash Course

If you only have 60 seconds before your test, read the cheat sheet. If you want to actually understand long calls so you stop second-guessing yourself in the testlet, scroll past it.

The 60-Second Cheat Sheet

For any long call position on the Series 7:

| Metric | Formula | Memory hook |

|---|---|---|

| Maximum loss | Premium paid | "You can only lose what you put in" |

| Maximum gain | Unlimited | Stock can theoretically rise forever |

| Breakeven | Strike + Premium | "Pay to play, then climb above strike" |

| Profitable when | Stock price > Strike + Premium | Above breakeven |

| At expiration | Exercise if stock > strike, else let expire | OTM calls expire worthless |

The trap question pattern: The exam will give you a stock price above the strike and ask for max gain. Candidates anchor on the number in the question and pick a finite answer. Max gain on any long call is always unlimited — full stop. The current stock price is irrelevant to that answer.

Worked Example (the one from the video)

Buy 1 XYZ January 50 call at 3. Stock rises to 58. What's the max gain?

- Strike: 50

- Premium paid: 3 (× 100 shares = $300 total cost)

- Breakeven: 50 + 3 = $53

- Profit at $58: ($58 − $53) × 100 = $500

- Max loss: $300 (the premium, if stock stays at or below $50)

- Max gain: Unlimited — not $500, not $800

The $500 is the current unrealized gain. The maximum possible gain is unbounded because XYZ could go to $100, $500, $5,000.

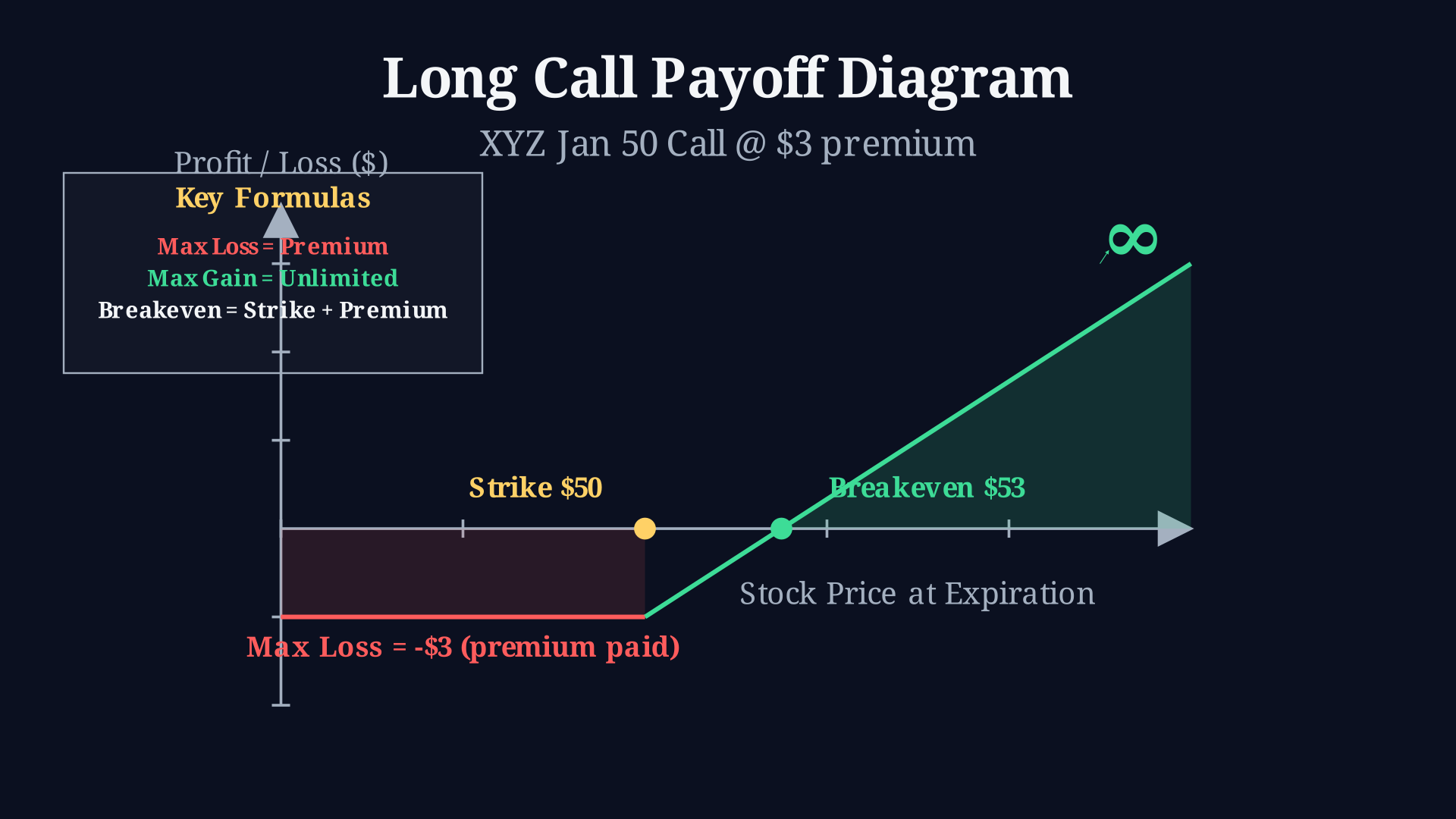

The Payoff Diagram

Three things to read off this chart instantly on test day:

- Flat line at −3 for any stock price ≤ 50 (the strike). You lose the premium and nothing more.

- Diagonal line crossing zero at 53. That's your breakeven: strike + premium.

- Arrow pointing up and to the right. That arrow is the entire reason long calls exist — there's no ceiling.

If you can sketch this diagram from memory in 15 seconds, you'll get every long-call question right.

Why This Question Trips People Up

The Series 7 writers know two specific traps work:

Trap 1: Conflating premium with max gain. The premium ($3, or $300) is the cost. Beginners see "$300" in the question and want to use it as the answer. It's the max loss, never the max gain.

Trap 2: Anchoring on the stock price given. When the question says "stock rises to 58," your brain wants to compute a number. But "max gain" asks about the theoretical maximum, not the current state. The only correct answer for any long call's maximum gain is unlimited.

The fix: when you see "long call" + "max gain," your hand should write "unlimited" before you finish reading the question.

How Long Calls Compare to Other Positions

The Series 7 will test you on all four basic positions in the same testlet. Here's the full comparison so you don't mix them up:

| Position | Max Loss | Max Gain | Breakeven |

|---|---|---|---|

| Long call | Premium | Unlimited | Strike + Premium |

| Short call | Unlimited | Premium | Strike + Premium |

| Long put | Premium | Strike − Premium (× 100) | Strike − Premium |

| Short put | Strike − Premium (× 100) | Premium | Strike − Premium |

Notice the symmetry: long positions cap your loss at the premium. Short positions cap your gain at the premium. Memorize the long call, then flip it for the others.

Common Series 7 Question Variants

Expect these phrasings on the actual exam:

- "What is the maximum potential gain?" → Unlimited (for any long call).

- "At what price does the investor break even?" → Strike + Premium.

- "What is the maximum loss?" → Premium paid × 100 (or just "the premium").

- "At expiration, what is the investor's profit/loss if the stock is at $X?" → If X ≤ strike, loss = premium. If X > strike, profit = (X − strike − premium) × 100.

- "Will the investor exercise?" → Yes if stock > strike (any amount), even if still below breakeven. Exercising recoups some of the premium; letting it expire recoups nothing.

That last one is sneaky — exercising at $51 on a $50 strike with $3 premium still loses you $2/share, but it loses less than letting the option expire and eating the full $3 premium.

The Mental Model That Sticks

Think of a long call as a lottery ticket with a refund window:

- You pay a fixed price (the premium) for the right to buy at a fixed price (the strike).

- If the stock takes off, you keep collecting upside forever.

- If the stock flops, you walk away — your "loss" is just the ticket price.

- The "refund window" is exercising before expiration if the stock is above the strike, even if you're still under breakeven.

That asymmetry — small fixed downside, uncapped upside — is exactly why long calls are tested heavily on the Series 7. The exam wants to make sure you understand that asymmetry well enough to advise a real client.

Practice Question

<details> <summary>Click for answer</summary>A customer buys 1 ABC October 75 call at 2. At expiration, ABC is trading at $74. What is the customer's profit or loss?

Loss of $200.

ABC ($74) is below the strike ($75), so the call expires worthless. The customer loses the entire premium: $2 × 100 = $200.

Note: even though ABC is only $1 below the strike, the customer doesn't exercise — exercising would mean buying at $75 to immediately sell at $74, plus eating the premium. Letting it expire just costs the premium.

</details>What's Next

This is one of ~40 options concepts tested on the Series 7. The most commonly missed (in order) are:

- Long call payoffs ← you're here

- Long put payoffs (coming soon)

- Covered call writing (coming soon)

- Protective puts (coming soon)

- Straddles vs. spreads (coming soon)

If this guide helped, the 60-second video version is here — same content, designed to lock the diagram into your memory before sleep.

Series7Labs builds short-form explainers and study guides for every question type on the FINRA Series 7. Free forever. No login. No upsells until you're ready for the full course.

Related: All Series 7 lessons · Why options dominate the Series 7 · About Series7Labs